Banking has evolved significantly over the years, but one fundamental aspect remains crucial for seamless transactions—ABA numbers. An ABA number, also known as a routing transit number, plays a vital role in ensuring that your money moves securely and accurately between banks. Understanding what an ABA number is and how it works is essential for anyone who conducts financial transactions, whether personal or business-related.

In this article, we will delve into the world of ABA numbers, exploring their significance, how they function, and why they are indispensable in the banking industry. Whether you're a beginner or someone who wants to deepen their knowledge, this guide will provide you with all the necessary information to navigate the banking system effectively.

As we progress, you'll learn about the history of ABA numbers, their structure, and how they impact various types of transactions. Let's dive in and uncover the intricacies of ABA numbers and their role in modern banking.

Read also:Julian Edelmans Weight And Height A Comprehensive Look At The Nfl Star

Table of Contents

- Overview of ABA Numbers

- History and Evolution of ABA Numbers

- Structure and Components of an ABA Number

- Common Uses of ABA Numbers

- How to Find Your Bank's ABA Number

- Security Measures Around ABA Numbers

- Differences Between ABA and Other Banking Codes

- Regulations Governing ABA Numbers

- Frequently Asked Questions About ABA Numbers

- Conclusion and Next Steps

Overview of ABA Numbers

An ABA number, or routing transit number (RTN), is a nine-digit code assigned to financial institutions in the United States. It serves as a unique identifier for banks and credit unions, enabling the routing of financial transactions accurately and efficiently. The American Bankers Association (ABA) originally developed this system in 1910 to facilitate check processing.

Why Are ABA Numbers Important?

ABA numbers are crucial for various banking activities, including:

- Direct deposits

- Bill payments

- Wire transfers

- Automated Clearing House (ACH) transactions

Without an ABA number, banks would struggle to identify the correct institution for processing transactions, leading to potential errors and delays.

History and Evolution of ABA Numbers

The concept of ABA numbers dates back to 1910 when the American Bankers Association introduced them to streamline check processing. Initially, these numbers were designed to simplify the manual handling of checks. Over time, with the advent of electronic banking, ABA numbers have become even more essential, supporting a wide range of digital transactions.

Key Milestones in the Development of ABA Numbers

- 1910: Introduction of ABA numbers for check processing.

- 1970s: Adoption of ABA numbers for electronic funds transfers.

- 1980s: Expansion to include Automated Clearing House (ACH) transactions.

Today, ABA numbers remain a cornerstone of the U.S. banking system, ensuring the secure movement of funds across different financial institutions.

Structure and Components of an ABA Number

An ABA number consists of nine digits, each serving a specific purpose:

Read also:Hilton Garden Inn Riverhead Your Premier Choice For Comfort And Convenience

- Digits 1-4: Federal Reserve Routing Symbol

- Digits 5-8: Institution Identifier

- Digit 9: Check Digit

How the Check Digit Works

The check digit is a mathematical calculation used to verify the accuracy of the ABA number. This ensures that the number is valid and correctly formatted, reducing the risk of errors in transactions.

Common Uses of ABA Numbers

ABA numbers are utilized in various financial transactions, including:

- Direct Deposits: Automating salary payments to employees.

- Bill Payments: Facilitating automatic payments for utilities, loans, and subscriptions.

- Wire Transfers: Sending money domestically or internationally.

- ACH Transactions: Supporting electronic fund transfers between accounts.

Which Transactions Require an ABA Number?

Any transaction involving the movement of funds between banks typically requires an ABA number. This includes setting up recurring payments, transferring money between accounts, and receiving payments from employers or clients.

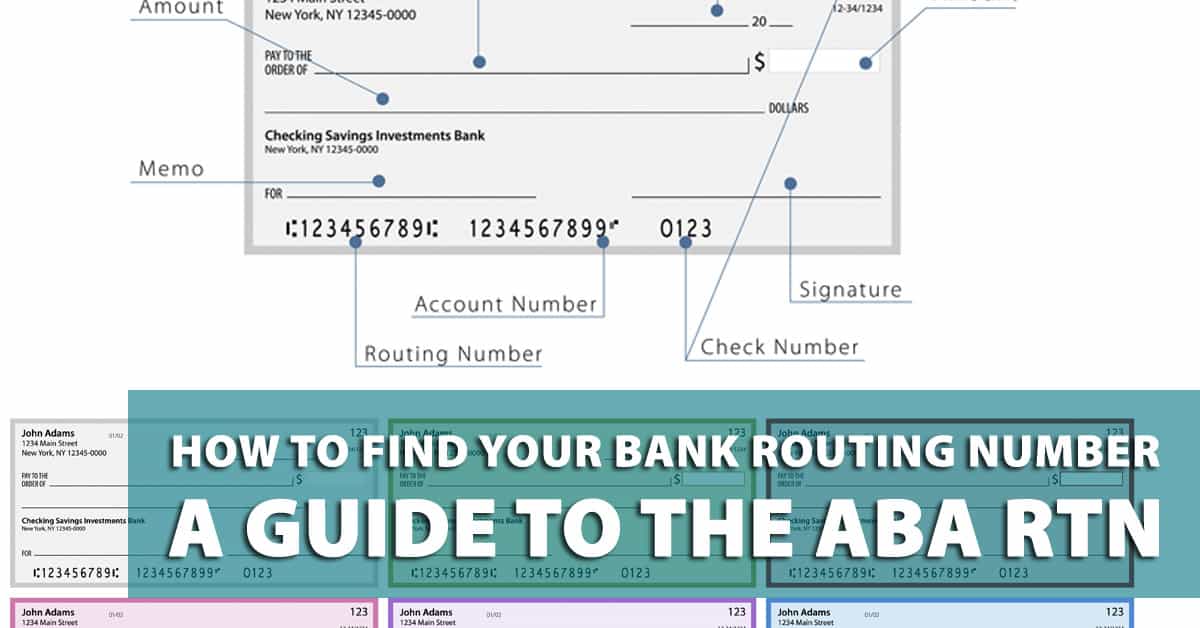

How to Find Your Bank's ABA Number

Locating your bank's ABA number is straightforward. Here are some common methods:

- Checkbook: The ABA number is usually printed at the bottom of your checks.

- Bank Statement: Most statements include the ABA number for your account.

- Online Banking: Access your account information through your bank's website or app.

- Bank Website: Many banks provide ABA numbers on their official websites.

Tips for Verifying an ABA Number

To ensure accuracy, always double-check the ABA number before initiating a transaction. Mistakes can lead to delays or incorrect processing of funds.

Security Measures Around ABA Numbers

ABA numbers are not sensitive personal information, but they should still be handled with care. Banks employ various security measures to protect these numbers from misuse, including encryption and secure authentication protocols.

Best Practices for Protecting Your ABA Number

- Keep your ABA number confidential unless necessary for a transaction.

- Use secure channels when sharing your ABA number online.

- Monitor your account activity regularly for any suspicious transactions.

Differences Between ABA and Other Banking Codes

While ABA numbers are widely used in the U.S., other countries employ different banking codes. For example:

- SWIFT Code: Used for international wire transfers.

- IBAN: International Bank Account Number for global transactions.

- Sort Code: Employed in the UK for domestic transfers.

When to Use ABA Numbers vs. SWIFT Codes

ABA numbers are primarily used for domestic transactions within the United States, while SWIFT codes are necessary for international transfers. Understanding the distinction between these codes is essential for ensuring smooth cross-border transactions.

Regulations Governing ABA Numbers

The Federal Reserve and the American Bankers Association oversee the issuance and use of ABA numbers. These organizations ensure compliance with industry standards and regulations to maintain the integrity of the banking system.

Key Regulations to Know

- ABA numbers must adhere to a standardized format.

- Financial institutions are required to register and update their ABA numbers as needed.

- Security protocols must be implemented to protect ABA numbers from unauthorized access.

Frequently Asked Questions About ABA Numbers

Q: Can I Use My ABA Number for International Transactions?

No, ABA numbers are specifically designed for domestic transactions within the United States. For international transfers, you'll need a SWIFT code.

Q: How Do I Know if My ABA Number is Correct?

You can verify your ABA number by checking your checkbook, bank statement, or online banking platform. Additionally, consult your bank's official website for confirmation.

Q: Are ABA Numbers Unique to Each Bank?

Yes, each financial institution is assigned a unique ABA number. However, large banks may have multiple ABA numbers for different regions or services.

Conclusion and Next Steps

In summary, ABA numbers are indispensable for facilitating accurate and secure financial transactions in the United States. Understanding their structure, uses, and security measures is crucial for anyone involved in banking activities. By following the best practices outlined in this guide, you can ensure the smooth processing of your transactions and protect your financial information.

We encourage you to share this article with others who may benefit from learning about ABA numbers. Additionally, feel free to explore more resources on our website for further insights into personal finance and banking. Your feedback and questions are always welcome in the comments section below!

Remember, staying informed about financial tools like ABA numbers empowers you to make better decisions and safeguard your assets. Thank you for reading, and we look forward to assisting you further on your financial journey!

:max_bytes(150000):strip_icc()/what-is-an-aba-number-and-where-can-i-find-it-315435_final-5b632380c9e77c002c9ef750.png)