Routing numbers and ABA numbers are essential components of banking operations, enabling seamless transactions and fund transfers. In today's digital age, understanding these terms is crucial for both individuals and businesses. Whether you're making a direct deposit, setting up automatic payments, or conducting wire transfers, knowing the differences between ABA vs routing numbers is essential.

This article will provide an in-depth exploration of ABA vs routing numbers, their functions, and their applications. We'll also discuss how they impact financial transactions and help you avoid common mistakes when using them.

By the end of this guide, you'll have a clear understanding of the distinctions between these two important banking elements and how they contribute to the smooth functioning of financial systems.

Read also:Who Is Colt Gray Unveiling The Remarkable Life And Career Of A Rising Star

Table of Contents

- What is an ABA Number?

- What is a Routing Number?

- ABA vs Routing Number: Key Differences

- History of ABA and Routing Numbers

- Functions of ABA and Routing Numbers

- How to Find Your ABA/Routing Number

- Common Uses of ABA/Routing Numbers

- Security Concerns with ABA/Routing Numbers

- Common Mistakes to Avoid

- The Future of ABA/Routing Numbers

What is an ABA Number?

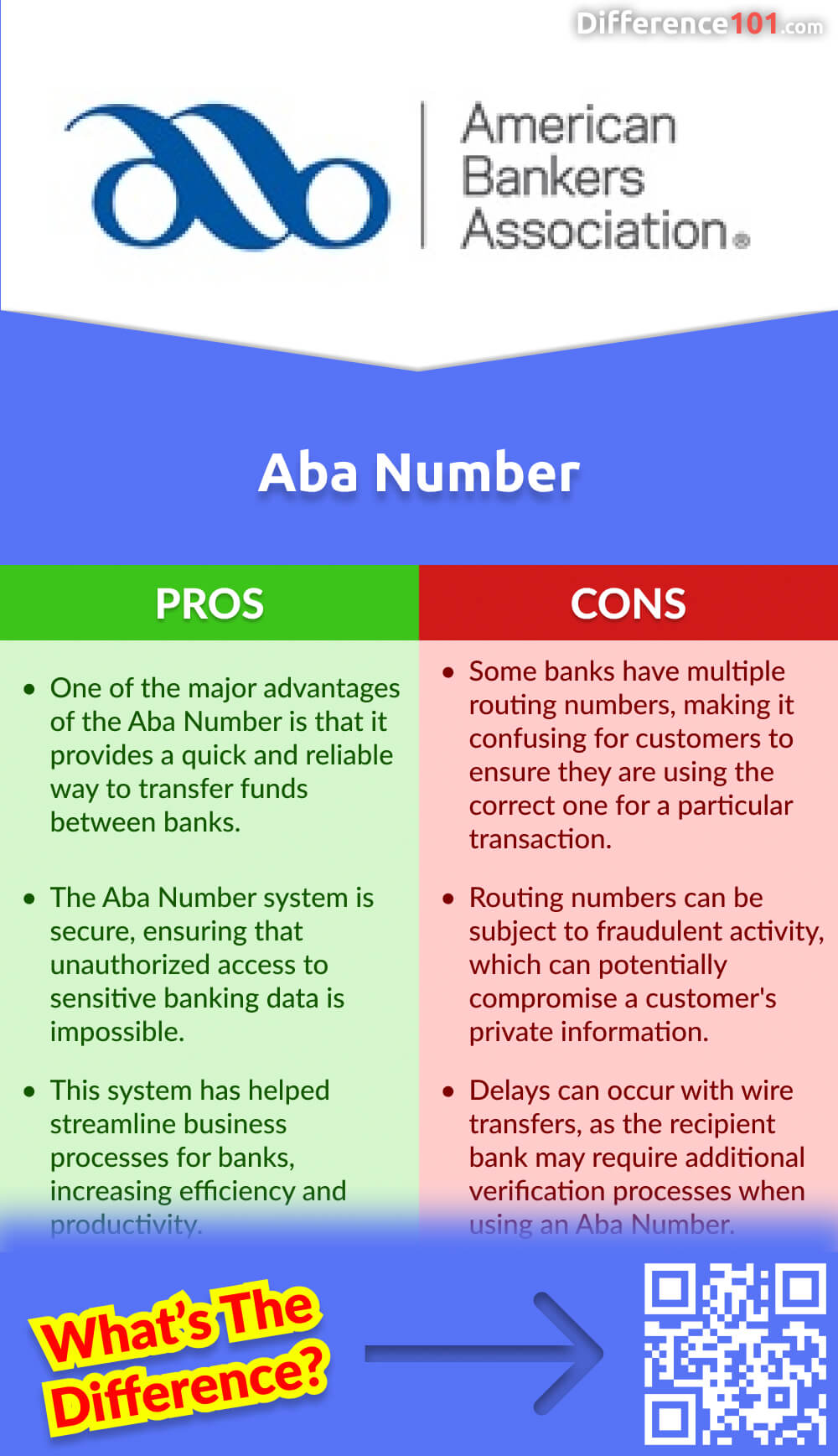

An ABA number, also known as the American Bankers Association routing number, is a unique nine-digit code assigned to financial institutions in the United States. It serves as an identifier for banks and credit unions, ensuring that transactions are routed to the correct institution.

Originally introduced in 1910, the ABA number was designed to simplify the check-clearing process. Today, it plays a vital role in electronic transactions, including direct deposits, automatic payments, and wire transfers. The ABA number is always located at the bottom of checks and is used by both domestic and international financial institutions.

Structure of an ABA Number

- First four digits: Federal Reserve routing symbol

- Next four digits: Financial institution identifier

- Last digit: Check digit for validation

For example, the ABA number 123456789 can be broken down into three parts: 1234 (Federal Reserve routing symbol), 5678 (financial institution identifier), and 9 (check digit).

What is a Routing Number?

A routing number is synonymous with an ABA number and serves the same purpose. However, the term "routing number" is more commonly used in modern banking contexts. It is a nine-digit code that identifies the specific financial institution where an account is held.

Routing numbers are crucial for facilitating various types of transactions, including:

- Direct deposits

- Bill payments

- Wire transfers

- Automated Clearing House (ACH) transactions

Types of Routing Numbers

There are two main types of routing numbers:

Read also:Is Jo Frost Married Exploring The Personal Life Of The Renowned Parenting Expert

- ACH routing numbers: Used for electronic transactions such as direct deposits and bill payments.

- Wire routing numbers: Used for domestic and international wire transfers.

It's important to note that some banks may have different routing numbers for ACH and wire transfers, so it's essential to confirm which number to use for each transaction type.

ABA vs Routing Number: Key Differences

While the terms "ABA number" and "routing number" are often used interchangeably, there are subtle differences between them:

- ABA number refers specifically to the original nine-digit code introduced by the American Bankers Association.

- Routing number is a more general term that encompasses both ABA numbers and other similar codes used in banking.

Additionally, routing numbers can vary depending on the type of transaction (ACH vs wire transfers), while ABA numbers are typically used for check processing.

Key Similarities

Despite their differences, ABA and routing numbers share several similarities:

- Both are nine-digit codes.

- Both identify specific financial institutions.

- Both are essential for facilitating financial transactions.

History of ABA and Routing Numbers

The history of ABA and routing numbers dates back to 1910, when the American Bankers Association introduced the ABA number to streamline the check-clearing process. At the time, banks and financial institutions faced significant challenges in processing checks efficiently, leading to delays and errors.

Over the years, the use of ABA numbers expanded to include electronic transactions, such as direct deposits and wire transfers. Today, routing numbers play a critical role in the modern banking system, enabling secure and efficient financial transactions across the globe.

Evolution of Routing Numbers

As technology advanced, the role of routing numbers evolved to accommodate new transaction types and payment methods. For example:

- The introduction of ACH transactions in the 1970s revolutionized electronic payments.

- The rise of online banking and mobile payments further expanded the use of routing numbers.

Functions of ABA and Routing Numbers

ABA and routing numbers serve several important functions in the banking system:

- Identifying financial institutions

- Facilitating check processing

- Enabling electronic transactions

- Ensuring secure and accurate fund transfers

Without these numbers, it would be nearly impossible to route transactions to the correct bank or credit union, leading to delays, errors, and potential financial losses.

How Routing Numbers Work

When you initiate a transaction, the routing number is used to determine which financial institution should receive the funds. For example, if you're setting up a direct deposit, your employer will use your routing number to send your paycheck to your bank account.

Similarly, when you make a wire transfer, the routing number ensures that the funds are sent to the correct recipient account at the specified bank.

How to Find Your ABA/Routing Number

Finding your ABA or routing number is a simple process. Here are a few methods:

- Checkbook: The routing number is printed at the bottom of your checks, usually in the first set of numbers.

- Bank statement: Your routing number may also appear on your monthly bank statement.

- Online banking: Most banks provide routing numbers on their websites or through their online banking platforms.

- Customer service: You can contact your bank's customer service department to request your routing number.

It's important to verify that you're using the correct routing number for the specific type of transaction you're conducting (e.g., ACH vs wire transfers).

Tips for Finding Routing Numbers

To ensure accuracy, always double-check the routing number before initiating a transaction. Additionally, consider saving your routing number in a secure location for future reference.

Common Uses of ABA/Routing Numbers

ABA and routing numbers are used in a variety of financial transactions, including:

- Direct deposits

- Bill payments

- Wire transfers

- ACH transactions

- Check processing

Each of these transaction types relies on accurate routing numbers to ensure that funds are transferred correctly and securely.

Examples of Routing Number Usage

Here are a few examples of how routing numbers are used in everyday banking:

- Setting up direct deposit for your paycheck

- Paying bills automatically through your bank account

- Sending money to family or friends via wire transfer

Security Concerns with ABA/Routing Numbers

While routing numbers are essential for financial transactions, they can also pose security risks if they fall into the wrong hands. For example, a fraudster could use your routing number to initiate unauthorized transactions or steal your personal information.

To protect yourself, it's important to keep your routing number confidential and only share it with trusted parties. Additionally, consider using two-factor authentication and other security measures to safeguard your bank account.

Best Practices for Security

- Never share your routing number unless absolutely necessary.

- Monitor your bank account regularly for suspicious activity.

- Use strong passwords and enable two-factor authentication.

Common Mistakes to Avoid

When working with ABA and routing numbers, it's easy to make mistakes that can lead to delays or errors in your transactions. Here are some common mistakes to avoid:

- Using the wrong routing number for ACH vs wire transfers.

- Entering the routing number incorrectly when initiating a transaction.

- Sharing your routing number with untrusted parties.

To minimize the risk of errors, always double-check your routing number and confirm its accuracy with your bank if necessary.

How to Avoid Mistakes

Here are a few tips to help you avoid common mistakes:

- Verify your routing number before initiating a transaction.

- Save your routing number in a secure location for future reference.

- Consult your bank's customer service department if you're unsure about which routing number to use.

The Future of ABA/Routing Numbers

As technology continues to evolve, the role of ABA and routing numbers may change. For example, advancements in blockchain and cryptocurrency could lead to new methods of identifying financial institutions and facilitating transactions.

However, for the foreseeable future, routing numbers will remain a critical component of the banking system, ensuring secure and efficient financial transactions for individuals and businesses alike.

Trends in Banking Technology

Some emerging trends in banking technology include:

- Increased adoption of digital wallets and mobile payments.

- Expansion of blockchain-based financial systems.

- Enhanced security measures for online banking and transactions.

Conclusion

In conclusion, understanding the differences between ABA vs routing numbers is essential for anyone involved in banking transactions. These nine-digit codes play a vital role in identifying financial institutions and ensuring secure, accurate fund transfers.

By following the tips and best practices outlined in this guide, you can avoid common mistakes and protect your financial information. We encourage you to share this article with others who may benefit from learning about ABA and routing numbers. Additionally, feel free to leave a comment or explore other articles on our website for more insights into personal finance and banking.